Has the Randomisation Experiment in FX Succeeded?

Posted by Colin Lambert. Last updated: October 18, 2023

Randomisation was seen as the key to “cleaner” FX markets when launched, but now, as Eva Szalay reports, the two primary venues appear to be taking a different attitude to its use

Ten years after it first appeared in currency markets, randomisation is facing a key test as the two primary trading platforms take opposing bets on the future.

CME-owned EBS Market announced recently that it’s rolling back some of the measures it’s had in place for the past decade, that were aimed at blunting the edge that speed gives to some traders, most notably latency arbitrageurs. This will include shortening batching windows for randomisation. At the other end of the spectrum, LSEG-owned Matching is doubling down on the practice, with plans to expand the use of randomisation to its NDF platform.

This means that the benefits of speed are on trial again – and the fast players seem to be winning, at least on EBS Market, which, by loosening some of its shackles on latency-focused players, brings the market full-circle on the issue. It also means, by voting for speed, the venue is signalling its priorities have changed from a decade ago.

“I can understand why they’re doing it, but I fear that the ecology is returning to what we’d seen before. My concern is that we’re doing a full 360 on more than a decade of evolution,” says the head of electronic trading at a top-tier bank.

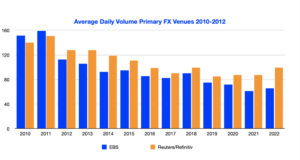

The stakes are high for both platforms, but the threat to EBS Market is possibly existential as it lacks the terminal business that its rival operates, especially in emerging market countries. Volumes have declined dramatically on both Matching and Market, to a level where a four-hour outage on EBS Market earlier this year caused very little distress to the market.

By opting to cut back on take steps favouring the fast set, the platform is fighting for relevance for the second time in a decade – but with what seems a directly opposing strategy.

One specific aspect of the strategy involves randomisation. EBS introduced the practise 2013 in response to the launch of the project currently known as ParFX and to stave off the threat of its key customers – banks – abandoning the then ICAP-owned venue in anger over the arrival – and perhaps even allegedly preferential treatment of – HFTs (one challenge being the popularity of EBS Prime amongst the bank’s prime broking teams).

After a couple of years of negotiations amongst banks, broker Tradition that had taken on the PureFX project, announced the launch of ParFX in April 2013, debuting randomisation as a major step in the fightback against the ever-escalating race for speed. EBS under then chief executive Gil Mandelzis responded by rolling out its own version of latency floors, with Reuters Matching eventually following suit in 2016.

Since then, randomisation, or latency floors, are established features of currency markets due to the thinking that allowing speed to dominate in trading will create unfair advantages for some companies with little benefit to end clients. But implementing these measures did little to arrest the slide in market share the two primaries experienced.

“Randomisation helped keep liquidity with the CLOBS for longer, without it I don’t think they’d be still around,” says a former trading head at a bank, who was instrumental in the creation of the PureFX project.

That Was Then, This is Now

But volumes on both primary platforms have declined dramatically in the past decade.

EBS told clients in its notification about the changes that the tweaks come “following prior communications and consultation with market participants.” Matt Gierke, an executive director on the leadership team for EBS markets, adds in an emailed comment that trimming the batching window to 1-3ms from its current 3-5ms will not have a major impact on outcomes.

“[The change] reflects that on the new more deterministic Globex platform, the vast majority of orders that join into batches tend to do so within a shorter timeframe than was the case previously and therefore we don’t need as long of a window to achieve roughly the same intended outcome,” Gierke says. “And at the same time, we get orders into the market with lesser delay as batches close slightly quicker.”

Part of the changes reflect shifts in the platform’s client base and ownership. A consortium of banks started EBS 30 years ago, before selling it to broker Icap in 2006. Despite the sale, banks remained the biggest clients of the platform in 2012, and their collective displeasure with the trading environment on Market forced a change at the top of the business and a new approach. Since 2018, however, CME Group owns the venue, and it caters primarily to a different crowd.

Saving EBS?

When Gil Mandelzis took the helm of EBS Market, the platform was still averaging above $100 billion worth of trades a day, but the trend was concerning. A few years into letting high frequency traders onto the platform, banks were in revolt as they struggled to adjust to the sharp-shooting style this new cohort brought to the table.

Led by some of the biggest heavy-weights, the consortium around the PureFX project was building momentum, with the mutual dislike of HFTs achieving the near-impossible task of uniting a handful of Wall Street’s finest around a common purpose. Michael Spencer, the chief executive of Icap swapped out David Rutter as EBS CEO, replacing him with Mandelzis, after tech glitches reinforced banks’ dissatisfaction with the trading environment on Market.

Mandelzis had earlier set-up and sold Traiana to Spencer’s Icap so he was familiar with the set-up of the company at least, but when he took over EBS, he walked into a firm that was at a crossroads.

Now CEO and founder of Capitolis, Mandelzis told The Full FX in an interview that as incoming chief of EBS in 2012, he had no choice but to act. The decline in Market’s volumes was alarming: by October that year average daily spot volumes were down 46% year-on-year to stand at $93 billion. The drops were much steeper than Matching, which saw some declines but still eked out some $120 billion worth of trades a day.

“Product development is not one and done, it was done in a specific context. Banks were enraged with EBS and five years after selling it to Icap they were seriously contemplating creating a new consortium with very broad participation. With all the big banks around the table, we needed to react in a certain way,” Mandelzis reflects.

Mandelzis had three goals: to make sure that the Pure project didn’t kill EBS, to slow down the deterioration of Market and to launch new products to compensate for the decline. The only way to do this involved cannibalising Market to some degree. “There was a recognition then that Market would continue to decline. We knew that second tier banks were only going one way and we had to stop a mass and fast defection. We knew EBS Market would continue to deteriorate, it was just a question of how fast,” he says.

Under Mandelzis EBS began a furious product launch cycle. It rolled back decimalisation before launching randomisation, made a push into electronic NDFs and introduced CNH to the platform. There was also the successful launch of EBS Direct, the disclosed platform which added further pressure on Market as volumes migrated away from the publicly visible venue.

Some of the launches were less successful, but EBS became the CLOB of choice for CNH, replacing Matching which had gained an early foothold, and the NDF platform continues to be a strong performer for the business. Thus, the flooding of the market with new products paid off to the extent that Market survived and the broad FX offering became a key part of the CME’s $3.2 billion acquisition in 2018.

Today Mandelzis says the strategy he and Spencer cooked up centred around EBS becoming a kind of Amazon of liquidity. He says that the steady market share loss of both Market and Matching are the market “voting with its feet” and choosing to trade at places where others can’t harvest information. Hence the rapid rise of internalisation ratios and the growth of disclosed trading. “I still believe that some of the speed strategies do not add real liquidity to the market and they’re a tax on society,” he argues. “I’m not sure that the things we talked about 10 years ago are any less relevant now.”

There is something in that statement, HFTs haven’t gone away – if anything, their role in financial markets has expanded and ballooned as they conquered asset class after asset class. Their market share on lit markets such as equities stands at 50%.

Ultimately, Mandelzis was brought in to steady a ship that while it may not have been sinking, was heading towards the rocks. EBS Market may be executing volumes that are at historical lows, but the broader business is hanging in around the $60 billion per day mark. “At the time, had we not done what we did, there was a real chance that PureFX would have been a real consortium<” says Mandelzis. “ParFX hasn’t become what it could have been and there is a very clear and direct correlation between that and what we did.”

Mandelzis told The Full FX in an interview (above) that in 2012 as incoming EBS CEO his priority was to stop a “mass defection” from the banks, who were in the process of forming a consortium around the Campbell Adams-orchestrated Pure project. Their uniting war cry was to stop the rise of HFTs, whose share of activity peaked in 2011 when EBS reduced its tick size, according to the BIS.

ParFX launched, but its aim of grabbing significant market share away from competitors does not seem to have succeeded – the platform does not publish volumes and owner Tradition does not break out revenues from the business, but sources familiar with its operation say that the ParFX platform continues to operate in the “low single-digit billions per day”.

There is also a general sense in the industry that the Pure/Par project had achieved what the banks wanted when EBS shifted its stance in 2012, and as such commitment to it diminished accordingly.

When asked to contribute to this article about the impact of randomisation, the ParFX management team said they were too busy to participate. “Thank you but not for us right now. As we are developing and extending the business we will look at media opportunities later in the year,” a spokesperson for the ParFX team said in an email.

Matching Goes the Other Way

Unlike EBS, the LSEG-owned Matching venue is doubling down on randomisation. As the company embarks on its multi-year re-platforming project, it plans to release a new version of the Matching platform with the same randomisation mechanism it uses today and it’s pushing the practice into other products.

“Randomisation mechanisms were an important innovation in market microstructure, and to this day remain especially appropriate on venues with all-to-all firm liquidity,” Hayden Melton, director, FX trading quantitative analysis at LSEG says in an emailed comment.

“We are launching a new venue, Cleared NDF Matching, in Singapore later this year and that venue will also implement this same randomisation mechanism because it too has all-to-all firm liquidity,” Melton adds.

He argues that randomisation abates the technological arms-race that traders are incentivised to engage in under equity market-like processing regimes, improves the quality of prices market makers are willing to post because they’re less afraid of snipers, and ensures fair treatment to participants.

But despite the practice becoming part of the FX ecosystem for a decade, randomisation has failed to turn ParFX into the “EBS killer” it set out to be. As the head of e-trading at the top tier bank says, “The success of ParFX hasn’t been the platform itself, but that its USP was copied by EBS and Reuters, and has been effective in creating a spectrum of fairness.”

The jury remains out, therefore, on whether randomisation has been a success in FX markets. The head of trading at a bank in the US, points out, “These platforms have long lost their relevance as far as trading is concerned, they’re now a data service to us,” which means volumes may not recover anytime soon. That said, the randomisation debate could be settled by the relative performance of Market and Matching in the coming years as they diverge in their approach and use of the practice.