What Happened at the Month-End Fix?

Posted by Colin Lambert. Last updated: July 8, 2025

In keeping with what was generally a quieter month in markets, potential savings from using a longer month-end fixing mechanism were lower than average, with some currency pairs offering similar market impact compared to a shorter window.

Five of the nine currency pairs tracked by The Full FX using data provided by Siren FX registered their lowest potential saving in 2025, with USD/CAD registering its lowest in the 50 months of tracking at just $15 per million. Every currency pair’s potential saving was below the long-term average, while only NZD/USD, USD/CHF and USD/SEK above the 2024 average – the latter being the quietest year of the four tracked thus far.

Generally speaking, Siren FX’ proxy calculations were close to the WM five-minute fixes, The Full FX checked rates with market sources to confirm as such, notably, USD/JPY would have provided larger savings that posted here, while EUR/USD would have provided a rare instance of the WM Fix offering a saving over Siren’s 20-minute methodology.

Those market sources, however, also observed that there was a “surprise move” in markets ahead of the WM window, rather than the dollar selling that was widely predicted and expected, dollar buying emerged into the window. This could, the sources suggest, have prompted speculative activity in the wrong direction from those accounts who often trade based upon market data from pre-hedging activity. Equally, other sources also point out that the dollar buying could simply have been a quirk of timing and that buying orders from non-fixing sources emerged.

To provide more context, the table below also presents projected dollars per million savings across a portfolio of different pairs using a correlation with the Fix calculation, depending upon how much flow was in the direction of the market, or “with the wind”. The rates used for the WM column are calculated using Siren’s proxy five-minute window, which utilises data from New Change FX, however The Full FX endeavours to check that they are a reasonable reflection of those published by the WM.

| June 30 |

| CCY Pair | WMR 4pm Fix* | Siren Fix | 100%** | 80% | 70% | 60% |

| EUR/USD | 1.17372 | 1.17373 | $9 | $5 | $3 | $2 |

| USD/JPY | 144.437 | 144.393 | $305 | $183 | $122 | $56 |

| GBP/USD | 1.37033 | 1.37029 | $29 | $18 | $12 | $6 |

| AUD/USD | 0.65532 | 0.65528 | $61 | $37 | $24 | $12 |

| USD/CAD | 1.36447 | 1.36445 | $15 | $9 | $6 | $3 |

| NZD/USD | 0.60707 | 0.60724 | $280 | $168 | $112 | $56 |

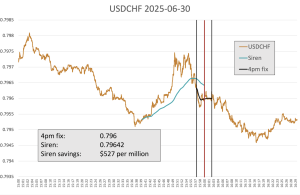

| USD/CHF | 0.7960 | 0.79642 | $527 | $316 | $211 | $105 |

| USD/NOK | 10.11969 | 10.11882 | $86 | $52 | $34 | $17 |

| USD/SEK | 9.53040 | 9.52629 | $431 | $259 | $173 | $86 |

| Average | $194 | $116 | $77 | $39 |

*According to Siren FX calculation using New Change FX data

** Savings are in dollars per million by percentage of correlation to the Fix flow. Blue cells signify a projected saving using Siren, Red cells a saving using WMR

The aforementioned confusion over the dollar’s direction is highlighted in the USD/CHF chart below, with steady dollar selling to the start of what would normally be the time when dealers start hedging their fixing risk. At that time, however, rather than continue down, steady buying emerged, followed by a sharper move higher as spec accounts probably got onboard.

Source: Siren FX

Notably, however, dollar selling re-emerged in the five minutes leading into the WM calculation window and continued into the first minute, before steadying. Dealing sources argue this reflects the actual hedging flow, which was lighter than normal – noting that the dollar continued lower post-fixing.

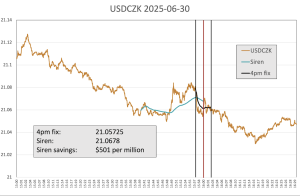

Every month, The Full FX is selecting an emerging market currency pair at random, and before the data is available, to broaden the analysis – this month the selected pair is USD/CZK. Data is again provided by Siren FX according to the same guidelines in place for the regularly reported currency pairs.

Source: Siren FX

The potential saving from the longer window remained substantial at $501 per million, but was only the fourth lowest in the past year. Again there was steady, if unspectacular, selling of dollar in the lead up to the pre-hedging period, followed by a short spurt of dollar buying, before selling into the WM window and beyond.