US Bank FX Swap Pricing Hurt by SA-CCR: BestX

Posted by Colin Lambert. Last updated: June 16, 2022

There have been hints that regulation is forcing banks’ to widen their FX swaps pricing, not least the Bank for International Settlements paper in 2020 which highlighted how G-SIB and other regulations were leading to wider spreads at quarter ends, and now analysis from State Street’s BestX has put a number on the impact of SA-CCR (standardised approach for counterparty credit risk).

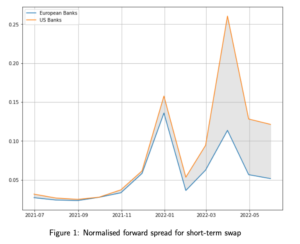

Source: BestX

The June 2022 edition of the BestX Expected Cost Monitor, look at the impact of SA-CCR on FX swap trading and finds that US banks in particular are being hit by the regulation. The analysis finds that the spread of short-term swap for US banks is 0.1bp wider than their European peers.

BestX calculates the normalised forward spread for FX swaps with a tenor of shorter than one year and to account for market conditions between the US and European countries, it normalised the spread by calculating the differences between the realised spread and the expected spread from the BestX Expected Cost Model.

The data show that the normalised spread for US and European banks started to diverge in January 2022 when SA-CCR rules were implemented in the US. Several European jurisdictions implemented SA-CCR in mid-2021, however, and there are suggestions that the widening of spreads by US banks is merely a “getting to know you” response to the regulation, as one FX swaps market source puts it, and that spreads could once again tighten as the reality of SA-CCR is better understood by the businesses.

The findings of the BestX analysis are backed up anecdotally by FX swaps traders spoken to by The Full FX, who point out that this comes against a backdrop of wider spreads generally. “We focus more on the impact of regulation than we ever did when pricing, and there is a cost that is now being passed through to the client,” says an FX swaps trader at a non-US bank in London. “However, volatility is also higher, and that is also showing up in spreads.”

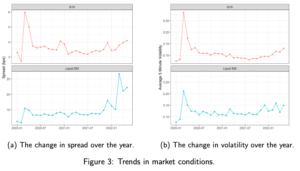

Source: BestX

Higher volatility is also a theme of the BestX report, which takes a look at changes in expected spot execution costs. The analysis finds there has been a slight increase in cost of G10 pairs, while in emerging markets, the increase is largely down to increased volatility in USD/TRY and European EM pairs.

The analysis also finds that average volatility across G10 and EM have increased recently, according to the percentage change in spreads versus volatility, and that activity is, generally, higher aside from a small group of pairs. This is also notable in the five-minute London 4pm fixing window, which is also analysed by BestX, and finds that while Fix spread and volatility have declined in EM and Scandi pairs since April, volatility over the fixing window has increased for European EM and liquid EM. Overall activity in the fixing window has declines except for liquid EM.