The Last Look…

Posted by Colin Lambert. Last updated: January 31, 2023

Does FX have a transparency problem, or rather, is one looming?

I was talking to someone last week who has a good insight into what the authorities are thinking and the point was made that if volumes on the CLOBs continues to deteriorate, those authorities would be concerned at the impact on market transparency.

This is not a new concern, it was first expressed by the BIS Markets Committee in 2018, and more recently it was mentioned as a possible issue in the latest BIS Quarterly Report into FX market conditions. It is also regularly raised by proponents of more transparent trading such as prop trading firms, who want to exploit their speed advantage.

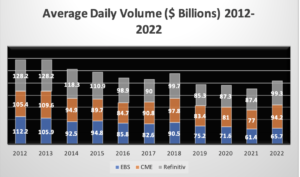

I think it is important to observe that since the BIS Markets Committee made their observation in 2018, actual notional volumes on two of the three venues often used for pricing data – CME, EBS Market and Refinitiv Matching – have hardly shifted (although EBS 2022 volumes were some 27% down on 2018). The problem is, I suppose, that the broader FX market has grown and they have not benefitted.

It is also probably noteworthy that 2022 was a very good year for CME and Refinitiv, and that the interim years were below 2018 levels – relative to volatility in the market in both years, it could be suggested they should be higher.

It’s at this point that I could make what some would consider to be a big call – that EBS Market and what is now LSEG Matching are close to the bottom in ADV terms – but I can’t. This is not because I think I’m wrong, rather that we have no idea on what the volumes on these venues are, they are wrapped up in the overall volume report related to multiple platforms in the group – breaking them out might be a start in raising transparency (at which point I give a hat tip to Cboe FX for breaking out firm ADV).

Anyway, back to the question of whether these platforms’ decline over the past decade is negatively impacting the market functioning and the authorities’ ability to effectively monitor them? The graph below shows the decline in all three from 2012, but this has to be placed in proper context. Those platform volumes are for spot only (CME is futures and options, the latter being about 10% of turnover as a rule of thumb) and using the regional FX committee data, spot turnover from April 2012 to April 2022 is only up 8.4%. I accept that is a rise, where the venues in question have declined, but it is significantly less than the 58% growth in volume across all FX products from those surveys. The growth has come in FX swaps, not necessarily spot.

So while there has no doubt been a decline, I am unconvinced that it is as severe as some would suggest. It should also be noted that the last decade has seen increased firm liquidity volumes at venues like LMAX Exchange and Cboe FX, both of whom offer market data (the latter has been publishing monthly data on firm liquidity since the start of 2020, the former only publishes annually).

I have argued before that LPs should be using a broader set of data sources, accepting that white noise and complexity comes with that, but I fail to see where there would be added complexity in the authorities using more sources as and when required. Given a decent run at it, I reckon my mother could find a level for most currency pairs that would reflect the current market, so it’s not about that – it’s about market structure when things go wrong.

But there’s the issue I have with complaints over market functioning – the FX market does function, and rather well at that. We have just had the busiest year for some time in terms of volatility and there were no accidents in FX. Yes, there were busy times when markets thinned out, but you could always get a fair price for your amount. This was, to accept a point made by my conversant, the first time we had sustained volatility and the primary CLOBs did not appear to benefit to any larger or smaller degree than the other venues, but across all venues, the market worked just fine.

Liquidity consumers should also not be complaining about a lack of transparency (to be fair, few do), because there are independent, third-party TCA firms that can provide a fair assessment of execution quality. Equally, the vast majority of those firms are multi-connected, either through an RFQ/RFS platform, or, increasingly it seems, aggregation.

I find it hard to support an argument that says the customer should have the protection of anonymity, but that the LP shouldn’t

This seems, then, to be a challenge primarily for the authorities, and whilst we shouldn’t under-estimate the scale of their problem I have bad news for them, as I suggested to my conversant last week. The fact is, liquidity consumers in the real economy (pension funds, corporates etc), don’t want transparency around their trades – that’s why they risk transfer or use an algo. I find it hard to support an argument that says the customer should have the protection of anonymity, but that the LP shouldn’t.

If the authorities want a more transparent FX market then they need to convince consumers that public markets are a better way to trade – good luck with that! It’s a sad fact that there are simply too many firms on these venues picking up information from trades in minimum size, who are then pricing or reacting accordingly. At that point, market impact goes through the roof and execution quality the floor. How do we change this? Well the venues could tighten up access and change how data is distributed but that could actually kill their business, meaning we will be back to square one.

It has been suggested to me in the past that the answer lay in the exchanges, but I struggle to see how a market structure with an exchange at the centre of it differs to a CLOB? The exchanges have a role to play, especially in swaps and derivatives, but spot? I am less convinced.

The solution, as far as I am concerned, is perhaps a bitter pill for the authorities to swallow, but swallow it they must. Unless there is to be global regulation on how the FX market operates, which is nigh on impossible, the structure will shift slightly, but remain the same – thanks mainly to consumer choice.

These authorities may have to work harder or take more data to sift through than is currently the case (although there is a point to be made that any “event” in FX will be highlighted in the primary venues’ data) and I don’t see this as a bad thing. As noted earlier, the FX market has faced multiple challenges in recent years, and has not only survived it has, as is often the case with FX in times of strife, thrived.