Is the US Sending the World A Message in FX Swaps?

Posted by Colin Lambert. Last updated: August 12, 2022

Ahead of the release of the eagerly-awaited Bank for International Settlements’ Triennial Survey of FX Turnover, The Full FX is taking a look at different aspects of the regional surveys, taken in the same month – in this article, what is happening in the FX swaps world?

Nowhere in the FX committee turnover surveys is there a divergence between centres as much as in FX swaps, for while the UK and Singapore in particular continue to hit new heights in notional turnover, in the US in particular, the opposite seems to be happening.

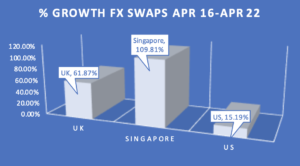

As noted in our report on the turnover surveys, Singapore has rapidly narrowed the gap on the US in terms of average daily volume (ADV) and while over the last year it has seen a sharp increase in spot activity, the sustained growth has been driven by FX swaps. Just one year previously, in April 2021, Singapore hit a new high for FX swaps turnover at $314.9 billion – roll forward (pun intended) one year and that figure stands at $454.3 billion. While the 44.2% annual growth is dwarfed by that of spot at 83%, this is coming off a much higher base and is all the more impressive for doing so.

In the UK at the same time, FX swaps ADV has risen from $1.58 trillion – itself a new high – to $1.69 trillion, a 7% rise. In the US over that time? Volume has declined by 12.6% from $357.1 billion to $312.2 billion.

While it should be noted that US turnover in FX swaps is higher than its historical average since the FXC started publishing data in 2005, this reversal of fortunes – especially against a backdrop of interest rate volatility, begs the question; why is it happening?

The simple answer is likely to be regulation. US banks in particular seem to have been hit harder and earlier by the SA-CCR (Standardised Approach to Counterparty Credit Risk) than their European and Asian peers. This has seen several US banks either pull back from the capital-intensive FX swaps market, or widen their pricing. These institutions also have considerable G-SIB (Globally Systemically Important Bank) requirements, meaning as their FX businesses grow, they have to add to their capital base. Rumours have been rife in markets over the past year that one US bank in particular has been paying especial attention to the G-SIB exposures and avoided what could be a huge capital charge by staying in a lower bucket.

With most of the capital regulations emanating from Basle, they have a global impact, and as such, what we are seeing now in the US could be a canary in the coal mine for the rest of the world in that banks in these regions will, at some stage, face the same challenges – albeit rarely on the G-SIB scale of the major US players.

If that is indeed the case, then we may be witnessing the golden age of the FX swaps market – and it could be followed by a winter. This would be of concern for customers seeking to use the FX swaps market to hedge their exposures, because anecdotal evidence is they will be receiving much wider spreads than they currently are.

Ironically, after nearly a decade of interest rate stability, this coincides with a rash of central banks maintaining a hiking cycle, although in no way in unison. This means FX swaps are likely to be an in demand product – the big question will be, is that demand going to be enough to sustain volumes hurt by wider spreads?