How Do the FX Platforms Compare to the BIS Data?

Posted by Colin Lambert. Last updated: November 9, 2022

If those spot FX platforms to publish monthly volume data were looking to benchmark themselves against the Bank for International Settlements (BIS) Triennial Survey data, most would come out of the exercise feeling pretty happy, with the vast majority seeing greater growth across the three-year span compared to the global data.

Of course, such an exercise for third parties is a little trickier mainly because of a lack of granularity in some firms’ data, and some platforms were clearly still very much in growth phase during the period, but in general, comparing April 2019 with the same month in 2022, it can be assumed that the platforms did well.

There will be a greater opportunity to assess performance when the BIS publishes more in-depth data and analysis, including execution style data, in its next Quarterly Bulletin, due in December, but across the nine venues tracked by The Full FX on a monthly basis, only one under-performed the global growth in spot trading.

Overall, spot volumes went up by $128 billion from April 2019 to April 2022, a 6.5% increase, as noted elsewhere, driven exclusively by volumes between Reporting Dealers. This would suggest that the primary venues, EBS Market and Refinitiv Matching, would have seen a significant bounce – one did, one didn’t – but that ignores how the BIS defines Reporting Dealer, which is very different to how relationships are defined in the market itself. Several Reporting Dealers are, in fact, very likely to be clients of a top tier liquidity provider, on some occasions via a platform.

BIS growth solid line (Only showing data from platforms that break out spot FX)

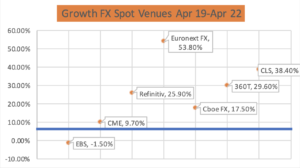

EBS is the only platform to see a decline in activity across the three-year comparison, by just $1 billion, or 1.5%. Although there is, anecdotally, a growing buy side presence on the firm’s platforms, it remains very much a bank-to-bank venue on both Market and Direct, its relationship-based venue. This means that, given the growth in Reporting Dealer activity (which almost certainly does not exist in a two-way, bilateral, environment, rather it is a one-way aggregation relationship), the data makes for sombre reading for EBS and its owner, CME Group.

When looking at Refinitiv’s performance it is much harder to ascertain the success, or otherwise, in Matching attracting this volume growth, because there is a lack of clarity in how the data is actually constructed and no breakdown is made between Matching and FXall volumes (as there is not between Market and Direct on EBS). Notwithstanding that, the overall Refinitiv data shows a 25.9% increase, or $21 billion, perhaps a reflection of more volume being traded outside the traditional G3 pairs. That said, informed sources suggest that the majority of the growth has come from FXall – something that reinforces the mystery of where the Reporting Dealer volume is being traded.

Away from those venues (and noting that CME’s FX futures and options suite saw growth of $7 billion per day, or 9.7%) the picture becomes very positive, although again it is important to note how some venues were still in “growth” mode, none more so that FXSpotStream. Over the three-year span FXSS saw volume growth of 91.4%, or just over $29 billion, however this period also saw it add member banks and launch algo trading on the service.

Another venue to see good growth, $18.6 billion or 59.6%, was Integral, however like FXSS, the firm reports volume data across all FX products, not just spot. That said, The Full FX understands that the majority of flow remains in spot for both firms.

Of those platforms with a longer existence, and who report just spot volumes, the story was fairly similar. Euronext FX had the largest notional and percentage growth at $8.6 billion and 53.8% (small caveat, April 2019 was the fourth quietest month for the platform in the period January 2017 to April 2022), while 360T grew by $5.9 billion, or 29.6%. The third venue in this bucket, Cboe FX, saw activity rise by $5.5 billion per day, or 17.5%.

A data point that is interesting, in that it suggests the growth in trading has come in a core group of currencies, is that of CLS Group’s daily settlement averages for spot transactions. Over the period, CLS spot volumes settled rose strongly, much stronger than the BIS data, by $115 billion or 31.9%.

Non-Spot Goes the Other Way

Although the data is much harder to disseminate, the high-level signs are that while non-spot activity has surged since 2019, the existing mechanisms for these products, which are limited, have not grown with them.

Again, some allowance has to be made for the fact that 360T has added a service dedicated to FX swaps, and also launched NDF trading (the latter data is not broken out in the headline BIS survey). This will have undoubtedly boosted the platform’s performance to a degree, however the data is still pretty impressive. From April 2019, non-spot volumes (using a constant exchange rate to convert from euros to dollars), non-spot volumes rose almost $37 billion, or by 59.5%.

This compares well with the impressive 17.4% increase in non-spot activity recorded by the BIS (which includes a 19.1% gain in FX swaps alone). Again though, it is worth noting that in notional terms, the global turnover in non-spot products rose by a fraction under $800 billion – proof, if needed, that there is still a lot of volume up for grabs.

The picture was less rosy for Refinitiv, which is much longer established in this field. Over the same period, non-spot volumes at the firm rose 6.5%, or by $22 billion – again though, the data doesn’t have the granularity to break out FX swaps data, or by venue.

Finally, on the non-spot data, another surprise involving CLS, one that suggests, in contrast to the spot data, activity has grown outside that service’s core currencies. Over the three-year period, outright forward and FX swap activity settled by CLS rose, but only by $115 billion, or 9.1%.

At the end of the day only those venues with access to more granular data will know how they are performing in the bigger picture. There is a lack of clarity as to where volumes are being traded, thanks to new venues entering the market (with varying degrees of success) and the lack of volumes from some existing providers.

One thing does seem clear, however, and that is more volume appears to be traded with LPs in competition, testimony to the rise in focus on best execution. It is probably as well for the platforms to avoid resting on their laurels, but as far as the latest BIS reporting period goes, they can at least give themselves a pat on the back.