BestX Publishes FX Global Code Algo Analysis

Posted by Colin Lambert. Last updated: October 25, 2021

A key element of the recent three-year review of the FX Global Code by the Global Foreign Exchange Committee was the greater use of templates to increase transparency for market participants. As well as templates for disclosures, a key release were two templates for algo due diligence and transaction cost analysis (TCA), thus allowing users of algos to better understand and compare their providers. Market participants were encouraged by the GFXC to review, and understand how and when they should use the templates.

To help clients better understand how its services reflect the principles in the FX Global Code and how its data fields stand up next to the templates, State Street’s BestX has published case studies, comparing how its algo input data fields compare with those in the GFXC templates.

The studies cover all input fields as well as some additional inputs which BestX receives for FX algos, then provides an overview of why each additional data point is useful and what metrics they are used for. The firm says the aim is to fully explain the benefits of providing as granular data as possible.

The paper sets out input fields for parent and child orders, as well as selected additional fields provided by BestX, for example, the reason for a reject, forward rate and points (when required), and any commission reflected in basis points. The firm also offers a field for executing parties acting on behalf of clients and for algo providers to differentiate between venues used that have signed up to the Code.

For individual trades the analytics are part of BestX’s Trade Inspector platform, however a feature of the service from the start has been the ability to drill down into the details, and that is highlighted by this latest paper. Users can view market arrival (either delivered by the algo provider or the time of the first fill); the algo name, to differentiate and analyse different strategies if they are used; and the urgency level, including changes throughout the parent order execution. “It’s important for BestX to receive the algo urgency in order to ensure when comparing/contrasting results, it is on a like for like basis,” the paper states. “For example, the same Opportunistic algo may behave very differently when set to ‘high’ urgency vs ‘low’ urgency – which is important to bear in mind both when interpreting results and selecting future algos.”

The provider fair value risk transfer can also now be analysed, BestX says buy and sell side participants have expressed an interest in comparing the performance not only against the risk transfer price provided by the firm, but also the one provided by the algo provider directly.

The execution type is also now available, BestX says that if provided, it can help visualisation of the Fill Chart; as is the platform of each child order execution, which can now be enriched with the actual location of the fill (i.e. LD4, NY4, SG1 etc). “Venue analysis is becoming increasingly important for algo users wanting to curate their liquidity, not only from a spread perspective, but also from a market footprint and liquidity type standpoint,” the paper observes.

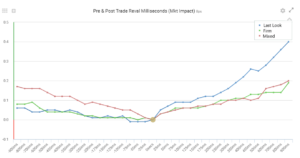

In line with the latest IA (Investment Association) and FXGC guidance, BestX also provides the capability to break out firm vs last-look liquidity in the platform whenever LPs tag the data accordingly in the input files. Once the “Liquidity Type” field is populated with one the 3 possible values (firm, last-look, mixed), BestX displays all the cost and impact metrics by each category.

One of the trickier aspects of the changes to the Code was greater transparency around the reason for rejects, an aspect that was, to a degree, skirted around in the Algo templates. With the GFXC firmly stating that additional hold times should be avoided when using last look, there are fears in the industry that some LPs may seek to obscure reasons for rejecting a trade to cover their continued use of latency buffering. This will, naturally, also be an issue for users of Algo execution strategies and to help better understand the issue, BestX is seeking to provide data inputs for reject reasons, including price tolerance, price improvement, credit check, latency and ‘other’. The firm says that some analyses are still under development and are dependent upon LPs providing the data to enable roll out.

Buy side sources spoken to by The Full FX have said that they expect their service providers to use the GFXC templates and to demonstrate their adherence to the Code’s principles in a proactive, rather than passive manner. This means, these sources clearly hope, that the BestX paper is one of several from providers in different areas of the industry that clearly explain how they are supporting the Code’s principles.

Algos are, to an extent, the ‘low hanging fruit’ in terms of Code adherence, so it will be interesting to see how things evolve from here, especially in the area of trade rejects.